Introduction

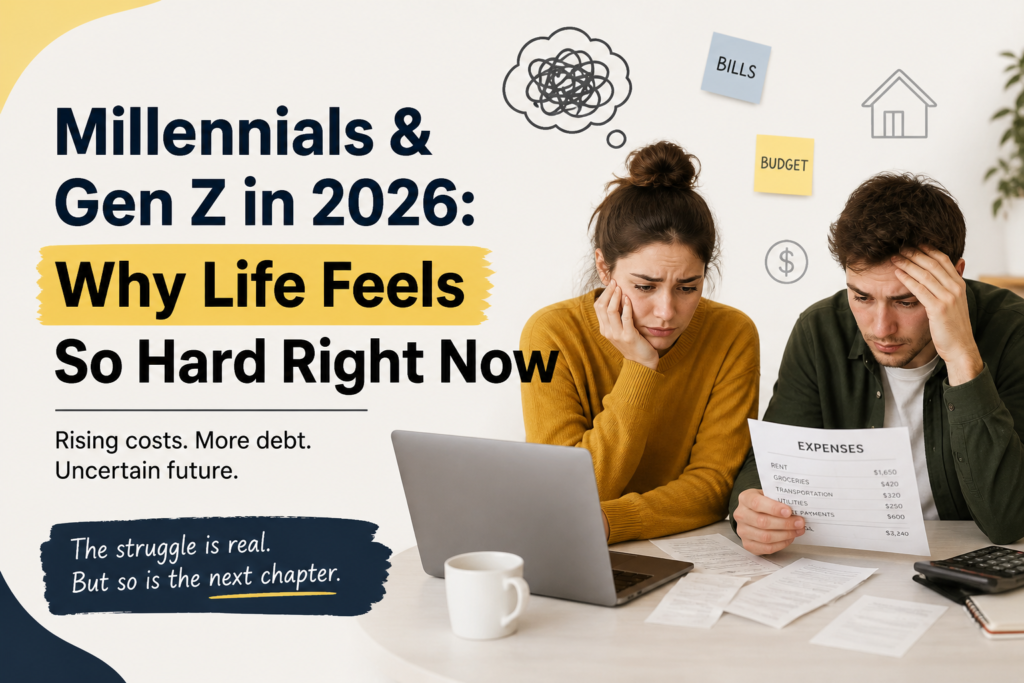

In 2026, Millennials and Gen Z are facing financial challenges that feel more intense and complicated than ever before. These generations are often described as educated, skilled, and adaptable — yet many are struggling to achieve financial stability.

Owning a home, building savings, or even managing everyday expenses has become increasingly difficult. Many young adults are working full-time jobs, some even juggling multiple income sources, but still feel financially stuck.

This raises an important question:

Why are younger generations finding it harder to get ahead, even when they are doing everything right?

The answer lies in a mix of rising costs, economic shifts, and changing expectations.

Table of Contents

Understanding Millennials and Gen Z

Before diving deeper, it helps to define these groups:

- Millennials: Born between 1981 and 1996

- Gen Z: Born between 1997 and 2012

Together, they form a large part of today’s workforce and consumer base. Their financial health directly impacts the broader economy.

However, their financial journey looks very different compared to previous generations.

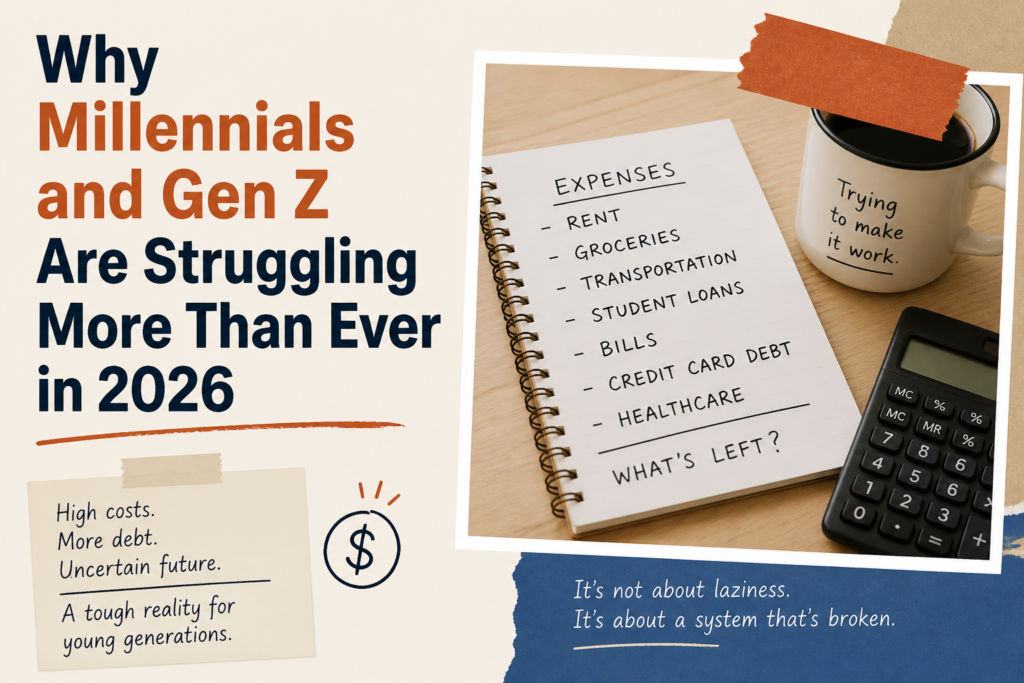

The Financial Reality in 2026

For many Millennials and Gen Z individuals, daily life includes:

- Managing rising expenses

- Limited ability to save

- Handling debt obligations

- Delaying long-term goals

Even those earning stable incomes often feel that their money does not go as far as it should.

The core issue:

The cost of living is increasing faster than income growth.

1. Rising Cost of Living

One of the biggest reasons for financial stress is the steady increase in living costs.

Everyday essentials such as:

- Rent

- Groceries

- Transportation

- Utilities

have become more expensive over the past few years.

Even small price increases across multiple categories add up quickly. This leaves less room for savings or discretionary spending.

For younger generations, this means:

More income is used just to maintain a basic lifestyle.

2. Student Loan Burden

Education is often considered a pathway to success, but it comes at a cost.

Many Millennials and Gen Z graduates carry student loan debt, which can take years to repay.

This creates several challenges:

- Reduced monthly disposable income

- Delayed financial independence

- Limited ability to invest or save

Even after securing a job, a portion of income is already committed to loan repayments.

3. Housing Affordability Crisis

Housing has become one of the biggest financial obstacles.

In many parts of the United States:

- Rent prices have increased significantly

- Home prices remain high

- Mortgage rates are elevated

As a result, many young adults:

- Continue living with roommates

- Stay with family longer

- Delay buying a home

Homeownership, once a key milestone of financial success, now feels out of reach for many.

4. Job Market Challenges

The job market in 2026 offers opportunities, but also comes with uncertainty.

Common issues include:

- Increased competition for high-paying roles

- Rise of contract or gig-based work

- Limited job security

Many jobs do not provide long-term stability or benefits such as healthcare and retirement plans.

This makes financial planning more difficult.

5. Growth of Credit Card Debt

To manage rising expenses, many young adults rely on credit cards.

While convenient, this often leads to:

- Accumulating debt

- High interest payments

- Long-term financial pressure

Small, everyday purchases can quickly turn into large outstanding balances if not managed carefully.

6. Impact of Inflation

Inflation continues to affect purchasing power.

Even when salaries increase slightly, they often do not keep up with rising prices.

This leads to:

- Reduced value of income

- Increased cost of daily living

Over time, this gap makes it harder to build financial security.

7. Social and Lifestyle Pressures

Social media has changed how people view success and lifestyle.

There is constant exposure to:

- Travel experiences

- Expensive purchases

- Ideal lifestyles

This creates pressure to maintain a certain image, even if it is not financially sustainable.

As a result:

- Spending increases

- Savings decrease

- Financial stress grows

8. Lack of Financial Safety Net

Many Millennials and Gen Z individuals lack sufficient savings.

Without an emergency fund, unexpected expenses such as:

- Medical bills

- Car repairs

- Job loss

can disrupt financial stability.

Even a small financial shock can create long-term consequences.

9. Delayed Life Milestones

Financial challenges are causing delays in important life decisions.

Many young adults are postponing:

- Marriage

- Homeownership

- Starting a family

These delays are not just personal choices — they are often driven by financial limitations.

10. Changing Nature of Work

The modern work environment is very different from the past.

There is a shift toward:

- Freelancing

- Remote work

- Gig economy roles

While these offer flexibility, they also come with:

- Irregular income

- Lack of benefits

- Financial unpredictability

This makes long-term financial planning more complex.

11. Increased Cost of Healthcare

Healthcare remains a significant expense.

Even with insurance, individuals often face:

- High premiums

- Out-of-pocket costs

- Unexpected medical bills

For younger individuals without strong coverage, this becomes a major financial burden.

12. Economic Uncertainty

Global and national economic shifts have created a climate of unpredictability. Factors such as market fluctuations, rapid policy changes, and volatile inflation trends affect everything from job stability to long-term retirement planning. This environment makes it significantly harder for younger generations to feel confident about their financial future, often leading to “financial paralysis” where long-term planning is sacrificed for immediate survival.

Factors such as:

- Market fluctuations

- Policy changes

- Inflation trends

affect job stability and financial planning.

This uncertainty makes it harder for younger generations to feel confident about their financial future.

Are Millennials and Gen Z at Fault?

It’s easy to assume that spending habits—often stereotyped as “avocado toast” or “lifestyle creep”—are the problem, but the data tells a different story. Most individuals are working longer hours, managing higher debt-to-income ratios, and trying to navigate a system where the “traditional” rules of wealth building no longer apply. The issue is not a lack of effort or discipline; it is an economic environment where the cost of entry into the middle class has doubled while wages have remained relatively stagnant.

How Younger Generations Are Adapting

Despite these challenges, Millennials and Gen Z are finding ways to cope.

Many are:

- Taking on side hustles

- Learning new skills

- Managing budgets more carefully

- Exploring alternative income sources

They are more financially aware and actively trying to improve their situation.

What Can Help Improve the Situation?

While there is no instant solution, certain steps can help:

For Individuals:

- Aggressive Budget Tracking: Use digital tools to monitor every dollar, focusing on “needs” vs. “wants.”

- Debt Prioritization: Focus on eliminating high-interest credit card debt first to stop the cycle of interest accumulation.

- Emergency Fund Micro-Saving: Even saving $10–$20 a week can help build a necessary safety net over time.

For Broader Change:

- Policy Support: Advocacy for more affordable housing developments and student loan reform.

- Wage Alignment: Encouraging corporate structures to adjust wages based on real-time inflation metrics.

- Enhanced Financial Literacy: Providing accessible, high-quality education on modern investing and tax strategies.

Small improvements in these areas can reduce financial pressure over time.

According to the latest data from the US Bureau of Labor Statistics, while certain sectors show wage growth, it often fails to offset the cumulative impact of inflation on essential goods.

Why This Topic Matters in 2026

Millennials and Gen Z are shaping the future of the economy.

If they continue to face financial challenges:

- Consumer spending may decline

- Economic growth may slow

- Financial inequality may increase

Understanding these challenges is essential for long-term economic stability.

Final Thoughts

The struggles of Millennials and Gen Z in 2026 are real, but they are not the result of failure.

These generations are navigating a more complex financial landscape, where rising costs, debt, and economic changes create additional challenges.

The reality is clear:

Financial success today requires more planning, discipline, and adaptability than ever before.

However, with the right strategies and awareness, it is still possible to move toward financial stability.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute professional financial, investment, or legal advice. Always consult with a certified financial advisor before making significant financial decisions.

Your Opinion Matters

Do you think Millennials and Gen Z are facing more challenges than previous generations?

Or is this simply a natural shift in how the economy works today?

Share your thoughts — your perspective matters.

Pingback: Earning More But Saving Nothing? The 2026 Money Trap Explained