Introduction

In 2026, the American Dream feels more like a financial trap than a success story. Despite a stabilizing labor market and steady employment figures, a startling reality persists: millions of Americans are living paycheck to paycheck in 2026. Even those earning what were once considered “comfortable” middle-class salaries find their bank accounts hitting zero just hours before the next direct deposit arrives.

But why is this happening? It’s not just a simple matter of “spending too much.” It is a perfect storm of systemic economic shifts, the evolution of consumer psychology, and a housing market that has decoupled from reality. In this detailed breakdown, we’ll explore the real reasons behind this financial pressure and provide a roadmap to breaking the cycle.

Table of Contents

What Does “Paycheck to Paycheck” in 2026 Really Mean?

Living paycheck to paycheck isn’t just a low-income struggle anymore. In 2026, “HENRYs” (High Earners, Not Rich Yet) are increasingly falling into this category. It means:

- Stagnant Wealth: You are working to pay for your past (debt) and present (bills), with nothing left for your future (investments).

- Zero Financial Buffer: An unexpected $500 car repair necessitates a credit card or a loan.

- Mental Health Strain: The “Sunday Scaries” aren’t about work; they’re about the bills due on Monday.

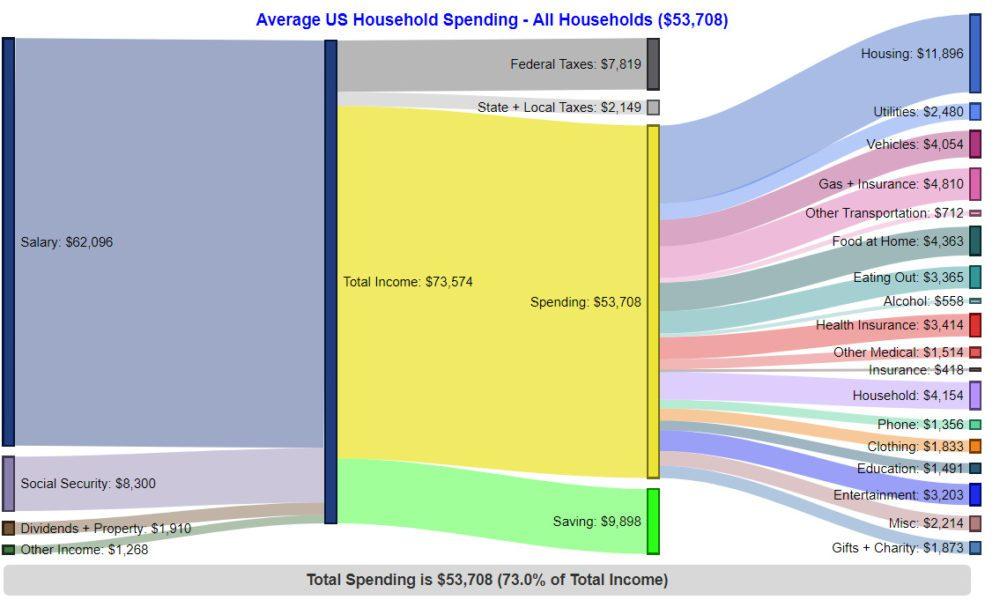

1. Rising Cost of Living in 2026

While the hyper-inflation of the early 2020s has cooled, prices never “reset” to pre-pandemic levels. Instead, we have entered a “New Normal” where the baseline cost of survival is significantly higher.

According to data from the Bureau of Labor Statistics, the weight of essential goods—groceries, utilities, and healthcare—now consumes a larger percentage of the average household budget than at any point in the last 30 years. When eggs and milk stay at premium prices while wages only see incremental 3% raises, the “Income vs. Reality Gap” widens.

👉 Example:

A person earning $4,000/month may spend:

- $1,800 rent

- $600 groceries

- $400 transport

- $300 utilities

- $500 insurance & bills

👉 Total = Almost entire salary gone

2. Housing Crisis & Rent Inflation

Housing remains the primary wealth-killer in 2026. The “30% rule” (spending no more than 30% of income on housing) is officially dead in most U.S. metro areas.

Interest Rate Lock-in: Many would-be sellers are staying put because they have 3% mortgage rates, keeping inventory frozen and prices artificially inflated.

The Rent Trap: Rent inflation has outpaced wage growth in 47 out of 50 states.

Institutional Buyers: Private equity firms continue to buy single-family homes, keeping supply low and prices high for first-time human buyers.

3. Credit Card Dependency & Debt Cycle

With the cost of living high, credit cards have shifted from “convenience tools” to “survival tools.” Total U.S. credit card debt has hit record highs in 2026.

- High-Interest Environment: With APRs hovering between 20-30%, paying only the minimum balance means you aren’t just paying for your groceries—you’re paying for them three times over in interest.

Many Americans:

👉 Use credit cards for daily expenses

👉 Pay minimum dues

👉 Fall into long-term debt cycles

This creates a situation where:

👉 Income = Expenses + Debt repayment

4. Subscription Culture (Hidden Money Drain)

It’s not just Netflix anymore. In 2026, we see “subscription fatigue” reaching a breaking point. From heated seats in cars to software for household appliances, the “pay-to-play” model of modern life creates a “death by a thousand cuts” for the American wallet.

Note: The average American now spends over $200 a month on digital subscriptions they often forget to cancel.h

Most people:

Don’t track subscriptions

Forget unused services

This silently drains income.

5. Lifestyle Inflation (Big Mistake)

As income increases, spending also increases.

This is called lifestyle inflation.

👉 Example:

- New job → higher salary

- Upgrade lifestyle → better phone, car, house

Result:

👉 No real savings despite earning more

6. Unexpected Expenses & Medical Costs

Healthcare in the U.S. is extremely expensive.

Even with insurance:

- Doctor visits

- Emergency care

- Medicines

👉 Can cost hundreds or thousands of dollars

One emergency = savings wiped out

7. Transportation & Insurance Costs

A major factor often overlooked in 2026 is the skyrocketing cost of Insurance.

Homeowners Insurance: Climate-related risks have made insurance in states like Florida, Texas, and California a massive monthly burden, sometimes equaling the mortgage payment itself.ng a car is necessary, not optional.

Auto Insurance: Increased repair costs for high-tech EVs and internal combustion vehicles alike have sent premiums soaring.

👉 Monthly transport cost = $300–$800+

8. Lack of Financial Education

Despite the wealth of information online, functional financial literacy is at an all-time low. Most schools still do not teach:

- The power of compound interest (both for and against you).

- How to navigate the 2026 tax code.

- The difference between “good debt” and “predatory debt.”

As a result:

- No emergency fund

- Poor money management

- High spending habits

9. Social Media Pressure & Spending Habits

The psychological pressure of “Lifestyle Creep” is amplified by social media algorithms. In 2026, the “Keeping up with the Joneses” has been replaced by “Keeping up with the Influencers.”

- Targeted Ads: AI-driven advertising is now so precise it can predict when you are most vulnerable to making an impulse purchase.

- Buy Now, Pay Later (BNPL): Services like Klarna and Affirm have “gamified” debt, making it feel like you aren’t spending “real” money.

👉 “Looks rich, but actually broke” is common in 2026.

10. Psychological Barriers to Escaping Paycheck to Paycheck in 2026

Breaking the cycle requires more than a spreadsheet; it requires a mindset shift. Many Americans suffer from “Decision Fatigue.” When you are constantly stressed about money, your brain’s executive function decreases, leading to poor financial choices. This “scarcity mindset” makes long-term planning nearly impossible because the brain is focused entirely on immediate survival.

Furthermore, the “You Only Live Once” (YOLO) economy remains strong. After years of global instability, many feel that saving for a future that feels uncertain is less important than enjoying the present. This cultural shift is a major reason why many stay trapped in the cycle of being paycheck to paycheck in 2026.

👉 “Hidden fees are also a major reason people struggle financially (Read here → Hidden Fees article)”

Strategies to Break the Cycle in 2026

If you feel trapped, you aren’t alone. Here is how Americans are pivotting:

A. The “Loud Budgeting” Movement

A trend gaining traction in 2026 is “Loud Budgeting”—vocalizing financial boundaries to friends and family. It removes the stigma of saying, “I can’t afford that dinner,” which reduces social spending pressure.

B. Radical Relocation

The rise of hybrid work has allowed a “Great Migration” to mid-sized “Zoom Towns” where the cost of living is 30% lower than in major hubs like NYC or SF.

C. The 50/30/20 Rule Refined

In 2026, experts suggest a tighter 60/20/20 rule for high-cost areas:

- 60% Essentials (Housing, Food, Utilities)

- 20% Debt Repayment/Savings

- 20% Lifestyle/Wants

Final Thoughts

Living paycheck to paycheck in 2026 is a systemic challenge, but your individual response is what determines your freedom. It requires a radical shift from passive consuming to active managing. By auditing your subscriptions, tackling high-interest debt, and ignoring the “digital noise” of consumerism, you can begin to build the margin you deserve.

To learn more about managing high-interest rates, you can visit NerdWallet for expert debt strategies. Financial stability isn’t about how much you make; it’s about how much you keep. Start small, stay consistent, and you can break the cycle of living paycheck to paycheck in 2026.

👉 With awareness and small changes, financial stability is possible. The key is:

- Smart spending

- Better planning

- Consistent savings

👉 If you found this helpful, check our latest US news updates here ➛ https://globalechousa.com/blog/

Pingback: Top Hidden Fees in the US 2026: Save Money by Avoiding These Charges

Pingback: Why Millennials and Gen Z Are Struggling in 2026: The Real Financial Crisis Explained

Pingback: 7 Best Budget Planners and Money Management Books in 2026 (Improve Your Finances Fast)

Pingback: 10 Hidden Money Habits That Keep People Broke

Pingback: Claude AI Down? Hidden Financial Risks & Proven Ways to Protect Your Income