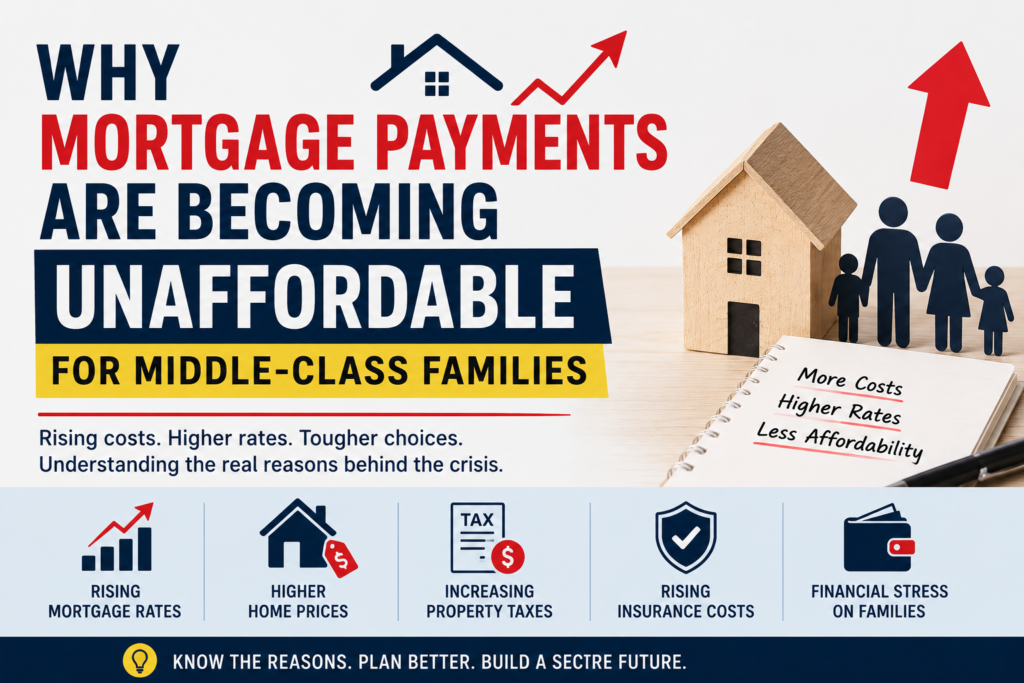

Mortgage payments are becoming unaffordable for millions of middle-class families across the United States, and for many households, the dream of homeownership is starting to feel further away than ever.

Just A few years ago, buyers could secure mortgage rates near historic lows. Today, rates remain significantly higher. According to current tracking data from the FRED Economic Data, the 30-year fixed-rate mortgage average stands firmly above 6%. Many Americans believed buying a home was one of the safest financial decisions they could make. Today, however, rising mortgage rates, increasing home prices, higher property taxes, and growing insurance costs are creating a financial burden that many families are struggling to manage.

Over the past year, I have spent time researching housing market trends, speaking with homeowners in online finance communities, and reviewing reports from economists and real estate experts. One thing became very clear: housing affordability has become one of the biggest financial concerns facing middle-class Americans in 2026.

For many families, the issue is no longer whether they want to buy a home. The question is whether they can realistically afford one.

Table of Contents

Why Mortgage Payments Are Becoming Unaffordable in 2026

The biggest reason mortgage payments are becoming unaffordable is simple: the cost of owning a home has increased much faster than household incomes.

While wages have risen in some industries, they have not kept pace with:

- rising home prices,

- higher mortgage interest rates,

- increasing insurance premiums,

- property taxes,

- maintenance costs,

- and overall inflation.

As a result, many families are finding themselves stretched financially even when earning what would traditionally be considered middle-class incomes.

Rising Mortgage Rates Are Increasing Monthly Payments

One of the biggest factors affecting affordability is mortgage interest rates.

A few years ago, buyers could secure mortgage rates near historic lows. Today, rates remain significantly higher.

The impact can be dramatic.

For example:

A family purchasing the same home today may pay hundreds or even thousands of dollars more each month compared to someone who bought during lower-rate periods.

Many buyers focus on home prices alone, but interest rates often determine whether a mortgage payment actually fits within a household budget.

Personal Research Observation

While reviewing mortgage calculators and housing discussions online, I noticed many first-time buyers were shocked when they saw how much higher monthly payments became after interest rate increases.

Even modest rate changes can dramatically affect affordability.

Home Prices Continue to Outpace Income Growth

Another major challenge is that home values remain elevated in many parts of the country.

Although some markets have cooled slightly, home prices remain far above pre-pandemic levels in many regions.

Unfortunately, income growth has not matched these increases.

Many middle-class families now face situations where:

- down payments are larger,

- monthly payments are higher,

- savings take longer to build,

- and qualifying for mortgages becomes more difficult.

This growing gap between income and housing costs is making homeownership increasingly challenging.

Property Taxes Are Rising Across America

Many buyers focus on principal and interest payments when calculating affordability.

However, property taxes can add hundreds of dollars each month to housing expenses.

Local governments often reassess property values, and higher home prices can lead to increased tax bills. This shifts the overall tax burden dynamically as outlined by public resource tools like the Freddie Mac Primary Mortgage Market Survey and municipal records.

For homeowners already managing tight budgets, these increases create additional financial pressure.

We often underestimate how much taxes contribute to the total cost of owning a home.

Home Insurance Costs Are Climbing

Insurance has become another major expense.

In many states, homeowners are facing:

- higher premiums,

- stricter coverage requirements,

- and reduced insurer availability.

Natural disasters, severe weather events, and rising rebuilding costs have pushed insurance rates higher.

Many homeowners report that insurance increases alone have significantly raised their monthly housing costs.

This is especially challenging for families who purchased homes at the upper end of their budget.

Why Middle-Class Families mortgage Are Feeling the Pressure Most

The housing affordability crisis is affecting many Americans, but middle-class families mortgage often caught in the middle.

Higher-income households generally have more financial flexibility.

Lower-income families may qualify for certain assistance programs.

Middle-class families frequently find themselves earning too much for assistance programs while still struggling to manage rising costs.

This creates a situation where many families feel financially squeezed despite working full-time and earning stable incomes.

Hidden Costs of Homeownership Most Buyers Ignore

One thing I consistently noticed during my research is that many first-time buyers underestimate the true cost of owning a home.

Mortgage payments are only part of the picture.

Additional expenses often include:

- maintenance,

- repairs,

- HOA fees,

- landscaping,

- appliance replacement,

- utilities,

- and emergency home repairs.

A roof replacement, HVAC repair, or plumbing issue can quickly cost thousands of dollars.

Many families are discovering that homeownership involves far more than the monthly mortgage payment.

The Housing Affordability Crisis and First-Time Homebuyers

First-time homebuyers face some of the biggest challenges in today’s market.

Many are struggling with:

- student loan debt,

- rising rent,

- expensive living costs,

- and limited savings.

Building a down payment while paying high monthly expenses has become increasingly difficult.

As a result, some younger Americans are delaying homeownership for several years or abandoning the idea altogether.

Are Americans Becoming House Poor?

A growing concern among financial experts is the rise of “house poor” households.

This happens when a large percentage of income goes toward housing expenses.

When mortgage payments consume too much income, families often struggle to afford:

- savings,

- retirement contributions,

- vacations,

- emergency funds,

- and everyday living expenses.

While homeownership can build long-term wealth, excessive housing costs may create significant financial stress.

How Families Are Adapting to Higher Mortgage Costs

Despite these challenges, many families are finding creative ways to adapt.

Some strategies include:

- Buying Smaller Homes

Many buyers are choosing smaller properties to keep payments manageable.

- Relocating to More Affordable Areas

Remote work has allowed some families to move to lower-cost regions.

- Increasing Down Payments

Larger down payments can reduce monthly mortgage obligations.

- Delaying Home Purchases

Some buyers are waiting for better financial conditions before entering the market.

These approaches may not solve every problem, but they can improve affordability.

What Experts Expect for the Housing Market

Predicting housing markets is always difficult.

However, many experts believe affordability will remain a major issue throughout 2026.

Several factors will influence future housing costs:

- mortgage rates,

- inflation,

- housing inventory,

- wage growth,

- and broader economic conditions.

While some markets may experience price stabilization, affordability challenges are unlikely to disappear overnight.

Personal Research: What I Learned

After reviewing housing discussions, mortgage calculators, homeowner experiences, and economic reports, one pattern stood out repeatedly.

Many families are not necessarily overspending.

Instead, they are facing a housing market that has changed dramatically in a short period of time.

People who once could comfortably afford a home are now finding that the same property requires significantly higher monthly payments.

This shift explains why so many middle-class families feel frustrated and financially stretched.

The issue is often larger than individual budgeting decisions.

It reflects broader economic trends affecting households nationwide.

Can Homeownership Still Be Worth It?

Despite affordability challenges, homeownership still offers benefits.

Owning a home can provide:

- long-term stability,

- potential equity growth,

- greater control over living space,

- and protection from rising rents.

However, buyers must carefully evaluate affordability before making major commitments.

Buying a home should strengthen financial stability, not create constant stress.

Final Thoughts

Mortgage payments are becoming unaffordable for many middle-class families because housing costs are rising faster than incomes.

Higher mortgage rates, expensive home prices, increasing insurance costs, and growing property taxes have combined to create one of the most challenging housing markets in recent years.

While homeownership remains an important financial goal for many Americans, today’s buyers must approach the market carefully and realistically.

For families navigating the housing affordability crisis in 2026, understanding the true cost of homeownership may be more important than ever.

Making informed decisions today could help protect financial stability for years to come.