Introduction

For decades, the Middle-Class Crisis in America represented stability, security, and opportunity. It was the foundation of the economy — a group of hardworking individuals who could afford a home, support a family, and still save for the future.

But in 2026, that reality is shifting.

Today, many Americans earning between $60,000 and $100,000 annually — traditionally considered middle-class income — are finding it increasingly difficult to maintain financial stability. Everyday expenses are rising, savings are shrinking, and long-term financial goals feel harder to achieve.

Many families are not necessarily earning less, but they are spending more just to maintain the same lifestyle.

So what changed? Why does it feel like the middle class is under pressure like never before?

Table of Contents

What Is Happening to the Middle Class in 2026?

The middle class isn’t disappearing overnight — but it is shrinking in terms of financial stability.

Many families who once lived comfortably are now:

- Living paycheck to paycheck

- Delaying major life decisions

- Cutting back on essentials

- Taking on additional work

The issue isn’t just low income. In fact, many middle-class households earn what would have been considered a “good salary” just a few years ago.

The problem is that expenses are rising faster than income.

This growing gap is the core of the middle-class crisis.

Why the Middle Class Is Struggling More Than Ever

1. Rising Cost of Living

Inflation continues to impact everyday life. Essentials like food, transportation, utilities, and basic services have become more expensive.

For example:

- Grocery bills have increased noticeably

- Electricity and utility costs are higher

- Fuel prices fluctuate frequently

Even small increases in multiple areas can significantly affect a household budget over time.

Many families are forced to adjust their spending habits just to keep up.

Groceries that once cost $100 may now cost $130–$150. Gas prices fluctuate, and monthly bills continue to rise. These changes may seem gradual, but they heavily impact household budgets.

2. Housing Affordability Crisis

The housing market is a primary driver of the Middle-Class Crisis in America. When mortgage rates and rent prices outpace average earnings, the stability traditionally associated with the middle class begins to vanish.

- Rent prices have increased significantly in major cities

- Home ownership has become less accessible

- Mortgage rates remain high

A large portion of income now goes toward housing alone, leaving less room for savings or other expenses.

For many families, owning a home — once a key part of the American Dream — feels out of reach.

3. Healthcare Costs

Healthcare remains one of the most expensive aspects of living in the US.

Even with insurance:

- Premiums are high

- Out-of-pocket expenses add up

- Emergency care can be costly

A single unexpected medical issue can disrupt a family’s financial stability.

This creates stress and uncertainty, especially for households already managing tight budgets.

4. Debt Pressure

Debt is another major factor affecting the middle class.

Common types of debt include:

- Credit cards

- Student loans

- Car loans

With higher interest rates, it becomes harder to pay off balances quickly.

As a result, many families find themselves trapped by::

👉 Minimum payments

👉 High interest over time

This cycle makes it difficult to build savings or invest in the future.

5. Wage Growth Not Keeping Up

While wages have increased slightly in some sectors, they haven’t kept pace with inflation.

This creates a situation where:

- Income rises slowly

- Expenses rise quickly

👉 Result:

Real purchasing power decreases

People feel like they are earning more, but in reality, their money doesn’t go as far as it used to.

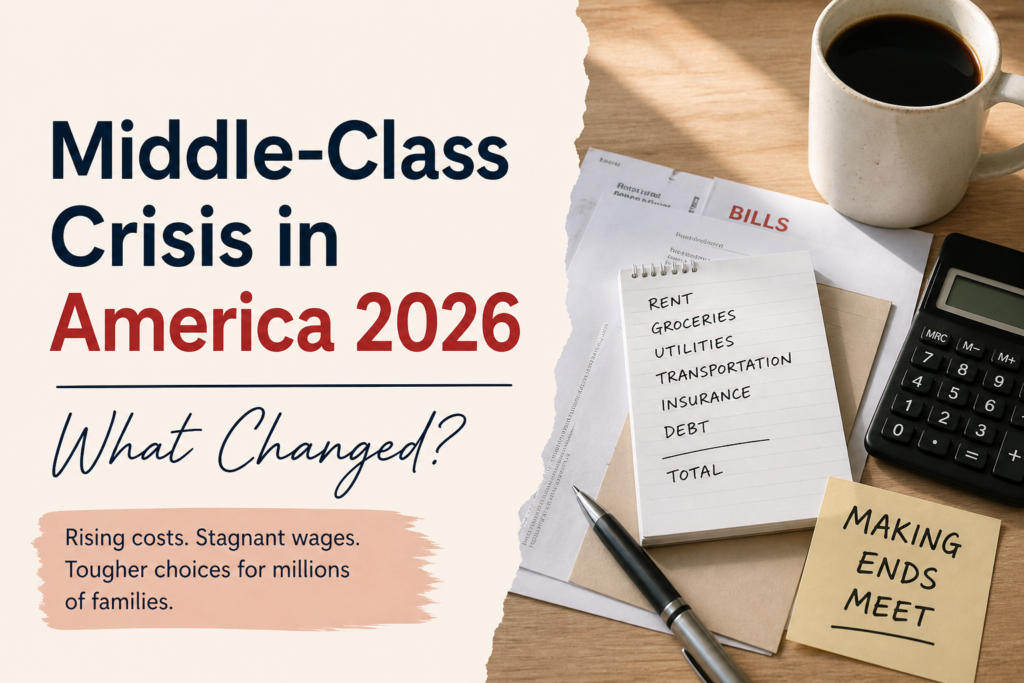

Income vs Expenses: The Real Gap

When calculating the gap between monthly earnings and rising costs, it becomes clear that the Middle-Class Crisis in America is a math problem that many families simply cannot solve without drastic lifestyle changes.

Imagine a household earning $80,000 per year.

After taxes, that income is reduced. Now consider monthly costs:

- Rent or mortgage

- Groceries

- Transportation

- Insurance

- Utilities

- Debt payments

By the end of the month, very little is left for savings.

This is why many middle-class families feel financially stuck. Even with stable jobs, they are unable to build wealth or prepare for the future.

The Psychological Toll: Beyond the Bank Account

The middle-class crisis in 2026 isn’t just a matter of numbers on a spreadsheet; it’s a growing mental health concern. For decades, being “middle class” provided a sense of psychological safety. Today, that safety net feels frayed.

- Decision Fatigue: When every dollar is accounted for, simple choices—like choosing between a child’s extracurricular activity or a car repair—become sources of significant stress.

- The “Status Anxiety” Shift: Many families are experiencing a “downward mobility” fear. The inability to provide the same lifestyle for their children that they had growing up creates a sense of generational guilt.

- Work-Life Imbalance: To stay afloat, the “Side Hustle Culture” has become mandatory. While this brings in extra income, it reduces the time families spend together, leading to burnout and a lower overall quality of life.

How Daily Life Has Changed for Middle-Class Families

The impact of this crisis is visible in everyday decisions.

Many households are:

- Choosing cheaper grocery options

- Avoiding dining out or entertainment

- Delaying vacations

- Postponing major purchases

- Taking side jobs or freelance work

In some cases, families rely on credit cards to cover basic expenses.

This shift in lifestyle reflects a deeper issue — financial security is no longer guaranteed, even for the middle class.

Geographic Disparity: Where You Live Matters More Than Ever

The crisis isn’t hitting every state equally. In 2026, we are seeing a “Great Migration” of the middle class as families flee traditional hubs for more affordable regions.

| Factor | High-Cost Hubs (NY, CA, WA) | Emerging Middle-Class Zones (TX, FL, NC) |

| Housing | Often exceeds 50% of take-home pay. | Stabilizing, though rising. |

| Remote Work | Decreasing as companies demand RTO (Return to Office). | High influx of remote workers seeking lower taxes. |

| Infrastructure | Aging systems with high utility costs. | New developments with better energy efficiency. |

Is the American Dream Still Possible?

The idea of the American Dream — financial independence, home ownership, and upward mobility — still exists, but it has become harder to achieve.

Younger generations, in particular, face unique challenges:

- High student loan debt

- Expensive housing markets

- Competitive job environments

Many feel that they must work harder for fewer rewards compared to previous generations.

While opportunities still exist, the path to success is no longer as straightforward.

What Can Be Done to Improve the Situation?

There is no single solution to the middle-class crisis, but several steps can help ease the pressure.

For Individuals:

- Budgeting and tracking expenses

- Reducing unnecessary spending

- Paying down high-interest debt

- Building emergency savings

For the Economy:

- Better wage growth

- Affordable housing policies

- Lower healthcare costs

Small improvements in these areas can make a significant difference over time.

Why the Middle-Class Crisis in America Matters in 2026

The middle-class crisis is not just a financial issue — it affects the entire economy.

When the middle class struggles:

- Spending decreases

- Economic growth slows

- Financial insecurity increases

Understanding the Middle-Class Crisis in America is essential because it serves as a primary indicator of the nation’s overall economic health and consumer stability in 2026.

Looking Ahead: Will 2027 Bring Relief?

As we analyze the future of the Middle-Class Crisis in America, the role of AI and legislative tax relief will be the deciding factors for recovery in 2027.

- AI and Job Automation: As AI matures, middle-management roles—the backbone of middle-class employment—are facing disruption. Those who adapt to technical roles may see wage growth, while others may face stagnation.

- Interest Rate Policies: If the Federal Reserve manages a “soft landing,” mortgage rates may dip, finally allowing the middle class to refinance and breathe easier.

- Legislative Support: There is a growing call for “Middle-Class Tax Relief” packages. Whether these become reality depends heavily on the political climate and upcoming fiscal policies.

Final Thoughts

The Middle-Class Crisis in America is not just a collection of individual financial struggles, but a systemic shift that requires careful analysis of wage growth and inflation. By understanding the root causes of the Middle-Class Crisis in America, families can better navigate the economic pressures of 2026, while policymakers can identify the necessary steps to protect the backbone of the nation’s economy.

The reality is clear:

👉 Many middle-class families are working harder

👉 But feeling less secure

Understanding this shift is the first step toward adapting and finding better financial strategies for the future.

What do you think?

Do you believe the middle class is shrinking, or is this just a temporary phase in the economy? Let us know your thoughts.

Let us know your thoughts — your perspective matters.

Pingback: Why Millennials and Gen Z Are Struggling in 2026: The Real Financial Crisis Explained

Pingback: Steam Machine Review 2026: Is It Worth Your Money or Just Another Expensive Gaming Upgrade?